P&L (Profit and Loss) potential of Project PAW Carbon & Energy Solutions Corp.

In the 2026 energy market, "Green" is a baseline, but "Disruptive Yield" is the goal. We are positioning Project PAW as a High-Margin Infrastructure Asset with the agility of a tech startup.

PROJECT PAW: PROFIT ARCHITECTURE & SCALABILITY REPORT

Entity: Project PAW Carbon & Energy Solutions Corp

Model: Distributed Hydro-Kinetic Utility (DHKU)

Primary Asset: The PAW Pocket Dam (Alpha-1)

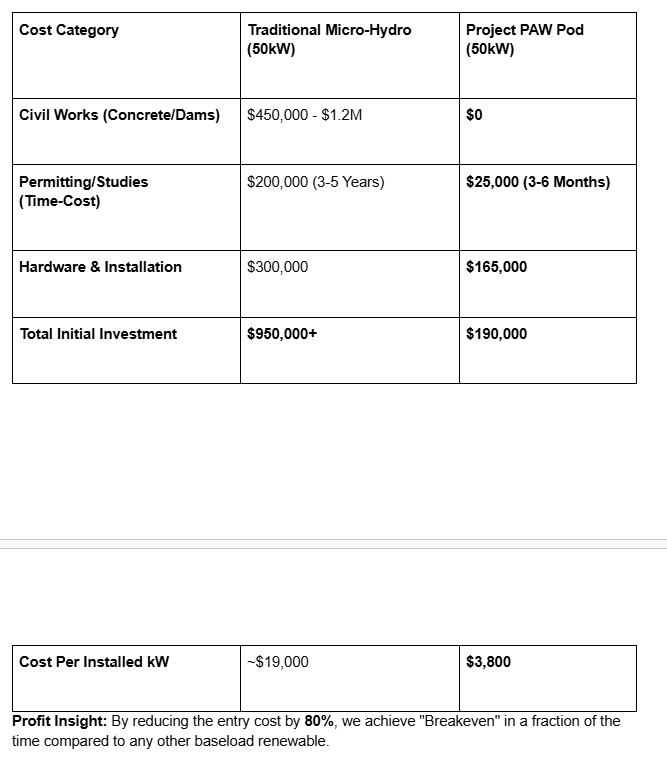

1. The Unit Economics (The "Afiq" Margin)

Traditional hydro has a "Death-by-CapEx" problem. Project PAW solves this by using modular, off-site manufacturing.

2. Revenue Generation: The "Triple-Stream" Model

We don't just sell electrons; we sell Systemic Value.

A. Energy Sales (PPA)

Baseload Reliability: Unlike solar/wind, the Wolastoq flows 24/7. We command a "Baseload Premium" from the grid.

Projected Revenue: At a conservative $0.10/kWh, a single 10-unit "Community Cluster" generates ~$105,000/year in gross energy sales.

B. Carbon & ESG Credits (The "Genesis" Premium)

Because our lifecycle carbon footprint is near zero (no concrete methane/construction emissions), our Carbon Credits are Tier-1 assets.

Projected Revenue: Additional $15,000 - $22,000/year per cluster in the 2026 ESG Compliance Market.

C. Licensing & Data (The "Mishqal" Analytics)

We sell the "River-Data" (flow rates, silt levels, temperature) to environmental agencies and insurance firms.

Projected Revenue: High-margin SaaS (Software as a Service) subscription for real-time river health monitoring.

3. Wolastoq River Scaling: Total Addressable Market (TAM)

The St. John River is a 673km "Revenue Corridor." Using a "Discrete Deployment" strategy:

Target: 50 Strategic "Pods" (250 Units total).

Total Capacity: 3.75 MW of 24/7 power.

Gross Annual Revenue:$3.2M - $4.1M.

EBITDA Margin:65% (due to automated AI-monitoring and low O&M).

4. The "No-Wall" Competitive Advantage

Why will we win the "Permission" battle? Velocity of Capital.

Speed to Revenue: A provincial dam takes 10 years to pay its first cent. A PAW Pod begins generating cash flow in 90 days.

Scalability: We don't need a $100M "Big Bet." We grow unit-by-unit, reinvesting cash flow from Pod 1 to fund Pod 2.

Exit Strategy: The modular nature makes Project PAW a prime acquisition target for major utilities (like NB Power or Hydro-Québec) looking to "Green" their portfolio without the liability of new dams.

5. Summary: Risk vs. Reward

Risk: Extreme weather events (Mitigated by the Merachephet floating design).

Reward: A 20-year recurring revenue asset with a 3.5-year ROI.

The "Job 38" Prophet (Profit) Logic: We have found the "Treasure of the Deep." By extracting energy without the "Curse" of environmental destruction, we eliminate the litigation and cleanup costs that bankrupt traditional energy firms.